YNAB vs Ranger: An Honest Comparison from a Former YNAB User

Joe Greve Founder of Ranger

Before we get into any comparison, let me be upfront: I’m the founder of Ranger, and I was a YNAB user for years before building Ranger. This isn’t an unbiased review - but I hope it’s an honest one.

I love what YNAB taught me about budgeting. The core methodology changed how my wife and I thought about money. But over time, I found myself frustrated with aspects of the platform: the learning curve was steep for friends I recommended it to, the price kept increasing, and I kept thinking “there has to be a simpler way to do this.”

So in 2023, we started building Ranger. Not to replace YNAB for everyone, but to create the budgeting app we wished existed - one that kept the power of zero-based budgeting but stripped away the complexity.

This comparison comes from someone who has lived in both worlds. I’ll be honest about where each tool excels and where it falls short. Whether you’re a budgeting beginner or a spreadsheet veteran looking to simplify your life, I’ll break down the key differences in cost, ease of use, user interface, and unique features.

It’s important to understand what makes both YNAB and Ranger special: both use zero-based budgeting.

Zero based budgeting can be confusing to explain, so instead, I’ll quote this excellent comment from Reddit:

The difference is that in a traditional budget you set limits for each category but if you go over, so what? Nothing happens. The limits have no relationship to the money you have right now. With a zero based budget you take the money you have right now and use that money to set your spending limits in each category. Go over in a category? You have to cover it from somewhere because that represents real money not just some vague aspiration. - u/Independent-Reveal86

This makes Ranger & YNAB so much more powerful for real-world budgeting, getting out of debt, saving for the future, etc.

(Want to learn more about how zero-based budgeting works in Ranger? Check out our guide to setting up budgets.)

(Updated as of November 2025)

Ranger is significantly more affordable, costing less than half of YNAB’s price. Over the course of a year, you’ll save $59 with Ranger’s annual plan compared to YNAB’s annual plan.

With Ranger, we committed to keeping pricing accessible. We’re self-funded, so we don’t have investor pressure to maximize revenue.

This is the big one. Both platforms use zero-based budgeting, but they differ in how they teach and implement it.

With all due respect to YNAB, they tend to have a bit of a “you just have to get it” type approach. Their UI + feature set is extensive, but not always intuitive. Either you understand it, or you don’t. And it can feel a bit alienating when you’re just starting out. Learning YNAB typically involves:

Personally, I had the advantage of using YNAB back when it was a piece of software you paid for once then downloaded 😅 - it was a pretty different piece of software back then, and you’ll frequently find old-school YNAB users who still hate the modern “cloud” based version.

YNAB can be effective. I’ve seen it make transformational changes in friends and family, but it has a pretty steep learning curve, and it’s easy to feel like you’re missing something all of the time.

With Ranger, we asked ourselves: “What if YNAB still had the great underlying logic, but without the learning curve + busywork?” We kept the zero-based budgeting methodology I loved from YNAB, but redesigned everything else to be intuitive:

YNAB offers a feature-rich interface with detailed budgeting tools, reports, and customization options. Some users appreciate the depth, while others find it:

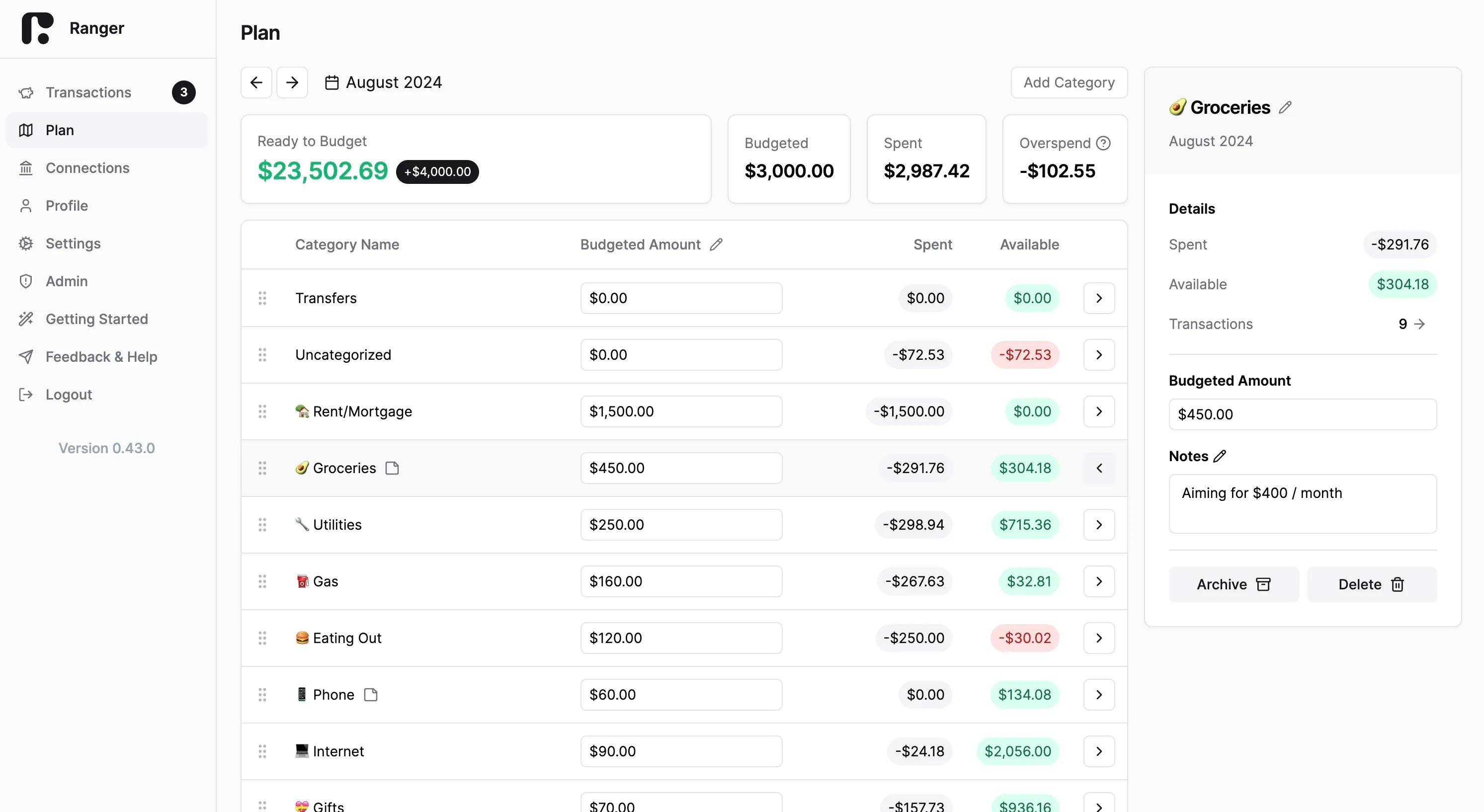

Ranger prioritizes speed, clarity, and modern design:

As both a developer and designer, I obsess over every interaction. One of my biggest frustrations with YNAB was waiting for pages to load and clicking through multiple screens for simple tasks. We built Ranger to feel instant. Every click should be satisfying, every page should load in milliseconds.

The Bottom Line: As of right now, YNAB provides more detailed reporting and analytics, which power users may appreciate. Ranger delivers a faster, more streamlined experience that reduces friction in your daily budgeting routine.

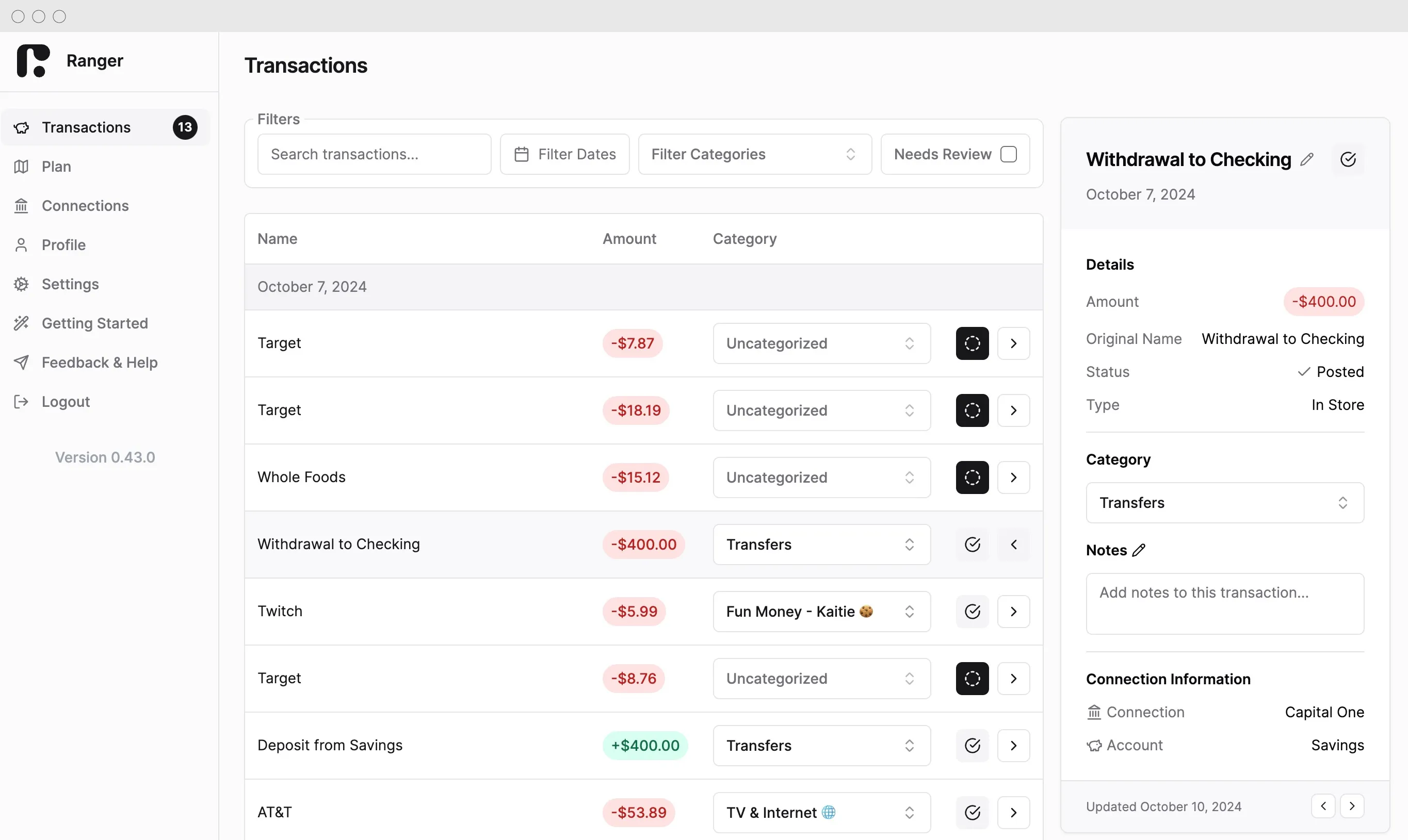

YNAB displays transaction information as it comes from your bank:

This is one feature I’m super proud of. When I was using YNAB, I’d see transactions like “AMZN MKTP US*2K4F71” and have no idea what I bought. I’d spend minutes digging through emails trying to remember if it was dog food or a book or something else entirely.

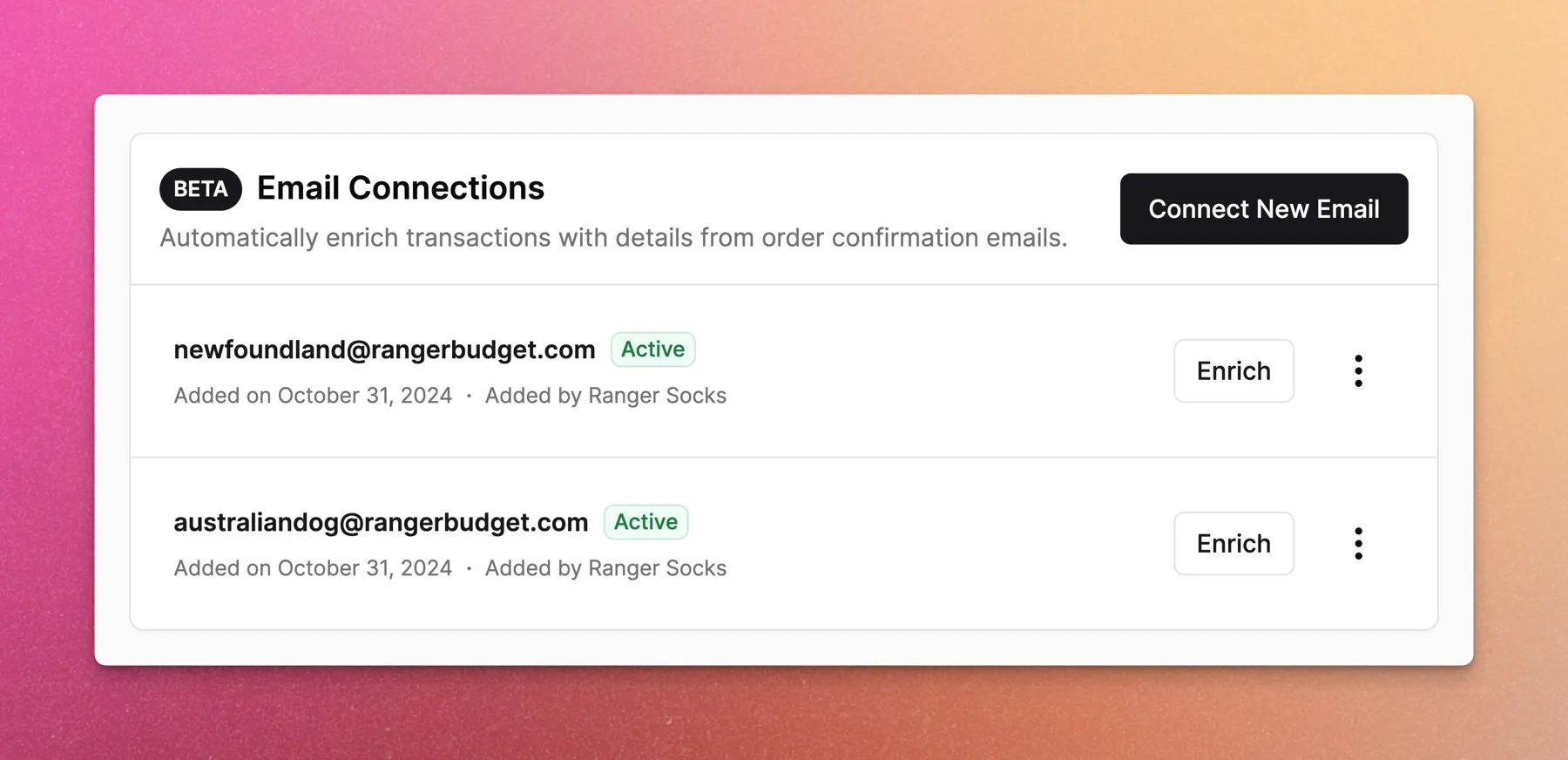

So we built something nobody else has: transaction enrichment (currently in beta):

Example: Instead of seeing “AMZN MKTP US*2K4F71”, you’ll see “Philips Sonicare Toothbrush Heads” - the actual product you purchased. This aligns with my earlier point that the best budgeting app should be the one you need to spend the least amount of time in. No more searching through emails to cross-reference what a purchase was.

💡 Note: Ranger’s enrichment feature is fully opt-in, and privacy-protecting. It only uses email data that you explicitly connect, and never shares or sells transaction details. Your data stays yours, always.

The Bottom Line: This is genuinely innovative. No other budgeting app (including YNAB) does this. If you’ve ever spent time investigating unclear transaction descriptions, you’ll love this feature. Learn more about transaction enrichment →

Learn more: Managing Transactions | Create Categories

YNAB might be the right choice if you:

Ranger might be the right choice if you:

Not yet - there’s no direct import tool currently. You’ll need to manually set up your budget categories and accounts in Ranger. I know this is a friction point for YNAB users considering a switch. The good news is that setup is quick (most people are done in 10-15 minutes), and the 35-day free trial gives you plenty of time to transition and decide if Ranger is right for you.

Ranger uses the latest Plaid APIs to connect to financial institutions, which supports over 11,000 banks and credit unions in North America. If your bank works with Plaid, it works with Ranger. See how to connect your accounts →

Yes, though it may defeat the purpose of simplifying your budgeting. Many users try both during the free trial period to see which one feels better for their workflow.

I can’t make promises about the future, but here’s some context: we’re self-funded and have no investors. We don’t have pressure to maximize revenue or chase aggressive growth. Our goal is to build a sustainable business that helps people, not to become billionaires. As long as we can keep the lights on and build great features, we’re happy to keep pricing where it is.

Not with the right tool! While the concept might seem complex, both YNAB and Ranger make it practical. The main difference is that YNAB requires more upfront learning, while Ranger aims to make it intuitive from day one.

There’s no universally “best” budgeting app - it depends on your needs, preferences, and budget.

Both YNAB and Ranger believe in the power of zero-based budgeting. They both help you give every dollar a job and manage your actual balance, not theoretical limits. The question is: which implementation of zero-based budgeting works better for you?

Choose YNAB if you want a comprehensive platform with native mobile apps and don’t mind the higher cost or learning curve.

Choose Ranger if you want an affordable, intuitive, fast budgeting tool that gets out of your way and lets you focus on your finances, plus innovative features like transaction enrichment.

Here’s my honest take as someone who used YNAB for years: YNAB is a great product. I used it for over ten years, and watched it evolve from downloadable software to the cloud-based solution it is today. But I also believe we can do better. We can make zero-based budgeting more accessible, more affordable, and more innovative.

I didn’t build Ranger to destroy YNAB - I built it because I saw an opportunity to help more people budget successfully. If YNAB works for you, that’s fantastic. If you’re looking for something different, I’d love for you to try Ranger.

The best way to decide? Take advantage of both free trials. YNAB offers 34 days, and Ranger offers 35 days - plenty of time to experience both platforms and see which one fits your financial life.

Start your 35-day free trial today - no credit card required.

Quick Links:

Disclaimer: This comparison is based on publicly available information and our experience with both platforms as of the time of writing. Features and pricing may change over time. We encourage you to visit both websites for the most current information.